By Janice Frampton, Senior Lean Consultant, Jean Cunningham Consulting

Is there a difference between "Lean accounting" and "accounting for Lean?" The two terms are often used interchangeably – and Lean accounting tends to be the term of choice for many Lean practitioners. But the difference between the two phrases is important and warrants further discussion.

Lean accounting relates to the application of Lean tools and techniques to finance and accounting processes, removing waste and streamlining processes to produce only what is needed as per the customer’s demand, whether that customer is external or internal.

Accounting for Lean involves modifying financial statements and reports to provide "plain English financial statements" that are usable by non-accountants while eliminating complexity and still complying with GAAP.

Attacking Waste in Finance

As implementers of Lean Beyond Manufacturing, Jean Cunningham Consulting continues to see more and more companies embracing Lean accounting, employing the principles of Lean across their finance enterprise by attacking waste in their key processes. These include accounts receivable/DSO, accounts payable, payroll, the financial close process, financial reporting, the audit process, and tax planning. Some major improvements have been made by companies that have taken this route, with significant reductions in waste across a multitude of processes.

Examples include reduction of the corporate monthly close process from 18 days to 1 day – a significant reduction that freed up financial resources to focus on value added work vs. "rear-window" work in closing the books. We’ve also seen significant improvement in externally focused metrics, for example a 20-day reduction in DSO – which translated to an incremental $120M in cash. This improvement came about with some very simple modifications to the process along with an effort to find the root cause of many of the receivable delays. The focus was placed on making corrections at the source versus finding fault with the customers, many of whom had legitimate complaints and cause for holding back payments.

We also find that companies implementing Lean accounting often find the need for more cross-functional process improvement events involving finance resources, even if the process is not "owned" by Finance. Examples of this include H/R processes such as onboarding and offboarding as well as in I/T and procurement, where finance is a key player in the removal of waste from the processes.

Identifying Wastes

The secret to waste removal from these core processes often depends on identifying the wastes – many of which we come to know and accept – and therefore dismiss as "just being part of the process." We become blind to these wastes simply because they have "always" been part of the process. Lean tools such as value stream mapping or process mapping are extremely beneficial in identifying waste in these back-office processes – particularly in identifying "Wait" time – which is generally the largest contributor to waste in a process.

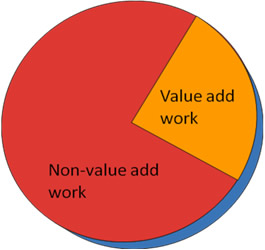

As is typical in process improvement, most participants focus on the area of the process they touch and feel – which is often times, the "value added" portion of the process. What they don’t see – and therefore continue to ignore – is the "non-value added" portion of the process – which generally contributes most of the time to any process. Figure 1 below identifies the time in a typical process. Most groups expend their efforts on the smaller piece of the pie that they are intimately familiar with instead of attacking the larger piece of the pie where all of the opportunity resides.

Figure 1 – Value Add vs. Non-Value Add Work Traditional improvement efforts focus on the value-added time. Where is the REAL opportunity?

Any activity that is non-value add is WASTE and is targeted for elimination.

So, while Lean accounting is well established today, accounting for Lean is still in its infancy in terms of companies migrating from using standard costs to account for their inventory and costs of production to embracing Lean methodologies to produce their financial statements. Although many companies talk about doing this, actual implementation requires a major mindset change from the top of the organization on down – educating the employee base and other internal stakeholders as well as external stakeholders, i.e. bankers, internal auditors, external auditors, etc., on what will change and what advantages those changes will bring.

Plain English Accounting Statements

A major change in this conversion is to move away from a standard-cost based Profit and Loss statement to one that is prepared using "Plain English." In other words, don’t fill the P&L with variances that don’t explain what happened with the business, but, instead, offer financial reports that allow the readers of the financial statements to make meaningful conclusions and decisions about the state of the business.

In the book, Real Numbers, co-authored by Jean Cunningham and Orest Fiume, six principles are followed when preparing Lean financial statements. They must:

Be usable by non-accountants

Eliminate complexity in presentation

Have higher assignable costs, lower allocated costs

Include both financial and non-financial information

Motivate the right decisions

Be compliant with GAAP

Below are two examples of a set of financial statements included in Real Numbers, the first (Figure 2) is a representative standard cost profit and loss statement. As you can see, the financial statement is full of variances, none of which are self-explanatory and none of which clearly point out a worrisome trend vs. a positive trend.

Figure 2 – Standard Cost Profit and Loss Statement

This Year

Last Year

Net Sales

100,000

90,000

Cost of Sales:

Standard Cost

48000

45000

Purchase Price Variance

-3000

10000

Material Usage Variance

-2000

5000

Labor Efficiency Variance

7000

-8000

Labor Rate Variance

-2000

9000

Overhead Volume Variance

2000

2000

Overhead Spending Variance

-2000

8000

Overhead Efficiency Variance

16000

-17000

Total Cost of Sales

64000

54000

Gross Profit

36,000

36,000

Gross Profit %

36%

40%

The second example (Figure 3) presents an alternative view of this same profit and loss statement – while complying with the Lean principles outlined above. You’ll note the word "variance" does not even appear on the alternative statement, but instead you see a very telling analysis that allows the reader to understand both positive and negative trends. Which one would you rather be presented with – or feel comfortable presenting?

Figure 3 – An Alternative Presentation

This Year

Last Year

+/- (%)

Net Sales

100,000

90,000

11.1

Cost of Sales:

Purchases

25300

34900

Inventory material (Increase)/Decrease

6000

-6000

Total Material Costs

31300

28900

8.3

Processing Costs:

Factory Salaries & Wages

13100

13500

0.7

Factory Benefits

7000

5000

40.0

Services and Supplies

2200

2500

-12.0

Equipment Depreciation

2000

1900

5.3

Scrap

2000

4000

-50.0

Total Processing Costs

26300

26900

-2.2

Occupancy Costs:

Building Depreciation

200

200

0.0

Building Services

2200

2000

10.0

Total Occupancy Costs

2400

2200

9.1

Total Manufacturing Costs

60000

58000

3.4

Inventory – Labor & Overhead (Increase)/Decrease

4000

-4000

0.0

Cost of Sales

64,000

54,000

18.5

Gross Profit

36,000

36,000

0.0

Gross Profit %

36%

40%

-4.0%

Engage the Finance and Accounting Organization in Lean

Whether it’s removing waste from your finance and accounting processes (Lean accounting) or putting an end to wasteful allocations, perpetual variance analyses and producing Lean financial statements (accounting for Lean), engaging the finance and accounting organization as part of your Lean journey is a critical step in ensuring that your entire enterprise reaps the benefits. Toyota has been successful with their Lean journey because Lean is a way of life at Toyota. It is part of their DNA. In order to share that same level of success, it is imperative that the finance and accounting organization understand both the requirements and benefits of Lean and become part of the core team that makes the Lean implementation a success.

Whether you are just embarking on your Lean journey or you are a seasoned proponent of Lean, ensuring your finance and accounting team is engaged and empowered is a key factor to moving that team away from the muda (waste) of transactional corrections and processing to the value added role of business partner.

About Jean Cunningham Consulting (JCC) Jean Cunningham Consulting (JCC) is a financial and process improvement consulting firm with clients throughout the United States. JCC specializes in "Lean Beyond Manufacturing," offering a full range of services that redevelop major processes into a Lean framework that sustains waste elimination and supports ongoing and long-term improvements. JCC is passionate about raising productivity throughout an organization and works directly with their clients to achieve high-impact, sustainable results. JCC offers custom tailored services to ensure optimization for each client, and has the expertise and experience to teach them the path to realize a fully productive and integrated Lean enterprise.